The second advanced estimates of national income, 2019-20 and the quarterly estimates of GDP for the 3rd quarter of 2019-20 was announced by the Ministry of Statistics and Programme Implementation (MOSPI) on 28th February, 2020. Let us first look at the performance based on the advanced estimates and then we will focus on the performance with respect to the quarterly estimates.

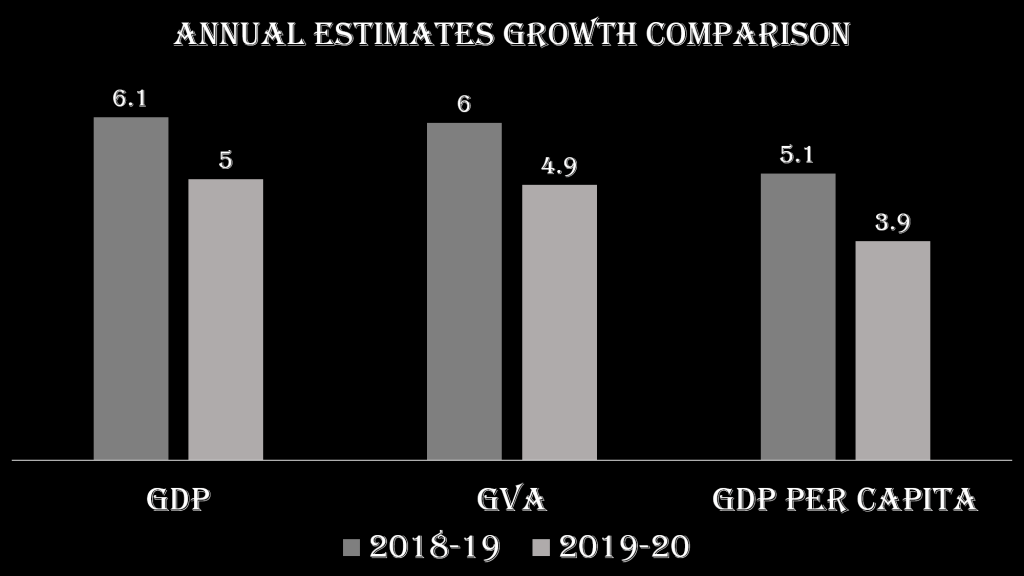

The advanced estimates puts the growth rate for 2019-20 to be at 5% as against 6.1% (Basis the 2nd revised estimates) in the previous financial year. This is significantly lower than the 7-8 % growth achieved couple of years back. The per capita GDP is predicted to grow by 3.9% as against 5.1% in the previous financial year. The per capita GDP is defined by GDP divided by the total population. So it reflects will be the GDP per person.

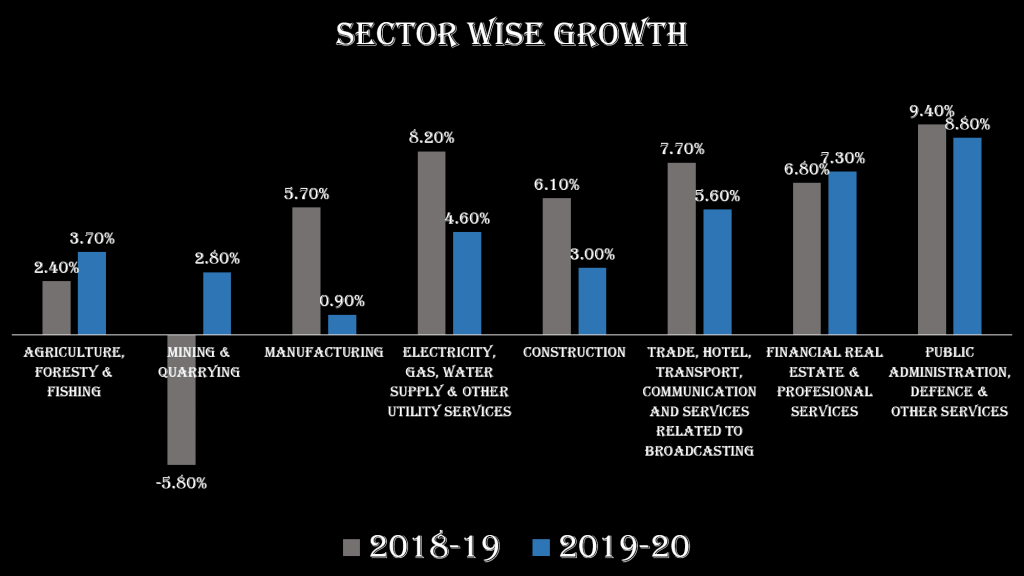

In terms of the sectoral growth, it is seen that apart of agriculture and mining, almost all other sectors have slower growth as per the advanced estimates in FY 2019-20 as against FY 2018-19. The higher growth in agriculture as per this report is a solace as it is the major source of income for a sizable section of population. But it has its own challenges in terms of farmers not getting correct prices and also the over dependence on this sector.

The drop is most severe in manufacturing sector. The slow growth in manufacturing and construction which employ a large section of population after agriculture is a big sign of worry. The unemployment rate has seen a record surge as per the latest reports on employment status.

Also the services sector which contributes the highest to India’s GDP has witnessed a slower growth as cited by the drop in growth rate for electricity, gas, water supply & other utility services and trade, hotel, transport communication and services related to broadcasting. The only silver lining is a marginal increase in the growth rate of financial , real estate and professional services. But the drop in the first two is much more severe than the increase in the growth rate of financial sector.

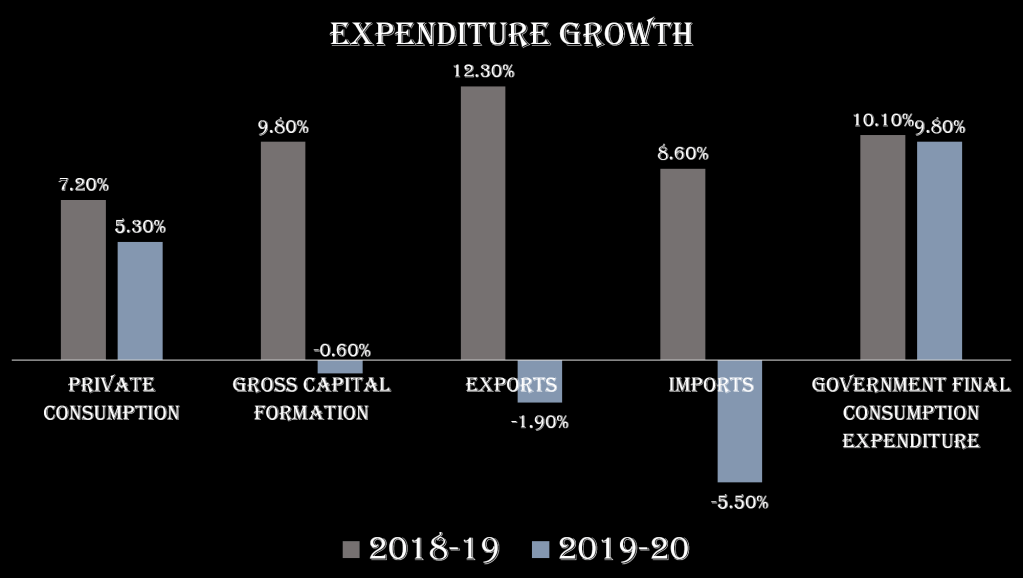

In terms of expenditure, all heads have witnessed a slower or negative growth in FY 19-20 as per the advanced estimates. There has been a slowdown in demand with a decline in growth rate of private consumption. Moreover given the challenges faced in the international market, exports show a negative growth in this financial year as against a massive positive growth in previous financial year. Also there is a significant drop in the imports as well. All of this is suggestive of a significant slowdown in demand.

A slowdown in demand would be detrimental for the businesses as this would mean lower revenue. This situation would mean a low or negative growth in investments. This is reflected by the negative growth in the gross capital formation in this financial year as against a higher growth rate in the previous financial year.

When economy faces a slowdown, what is needed is a surge in government spending as per the prescription suggested by the Keynesian economists. But what we see is a drop in the growth rate of government final consumption expenditure as per the advanced estimates. The government has faced with the need of more funds and we have seen a transfer from the reserves of RBI to the government. But along with this transfer the government also had to announce corporate tax cuts to get in more investments and what this means that the government has less funds to spend. Also there has been a lot said with the central government not giving states their due of the GST revenue.

Let us now look into the performance of Q3, FY 19-20 as being reported by the government. It must be noted here that the government revised the quarter one and quarter two growth estimates upwards. The Q1 estimates was revised to 5.6% as against 5% reported earlier. The Q2 numbers was revised to 5.1% from 4.5%. As per the estimates reported, the Q3 growth numbers stood at 4.7%. This would mean the growth rate in the third quarter is the lowest in the last 6 years. Moreover as compared to previous financial year, there is a slow growth in all three quarters in this financial year.

As is seen in terms of the advanced estimates, apart from agriculture, mining and financial services sector all other sector has witnessed a slow or negative growth in quarter three, this financial year as compared to the same quarter in the previous financial year. The drop in the growth rate of the people intensive sectors like manufacturing and construction is very severe with manufacturing witnessing a degrowth.

In terms of expenditure growth, there has been a decline in growth rate in terms of all heads except for government expenditure in Q3, 2019-20 as compared to same quarter, previous year. The decline in private consumption was much sharper in previous quarter.

In terms of gross capital formation, when we compare quarter on quarter growth, it is seen that as compared to quarter 1 there has been over 9% decline in gross capital formation in quarter 2 in this financial year. In quarter 3, there is around 3.7% growth in capital formation as compared to quarter 2. One must remember that the corporate tax reduction was announced in the middle of Q2. So is this rise in q3 as compared to Q2, due to this corporate tax cut. It must be noted in this respect in previous years when one compares quarter on quarter growth, there has been close to 5% growth in gross capital formation in Q3 as compared to Q2. So one really cannot attribute this fully on the corporate tax cut.

So in a nutshell with the revised estimates of quarter one and two, the Q3 performance seems to be the worst till now. IPD has reported that IIP, Core sector growth rate and credit to different sectors has shown a decline in Q3 as compared to Q2. Only in terms of personal credit there has been a marginal growth. So the GDP numbers seems to be inline with the quarter 3 performance being the worst among the three quarters of this financial year. The core sector growth in January has shown a positive growth after many months. It needs to be seen whether this trend continues in the coming months. If this trend continues, we can see some recovery in Q4.