The official growth figures for Q3, 2020 is to be released in the next few days. The revised estimates for the overall FY 2019-20 growth which was released in Jan, 2020 showed a 5% growth for the financial year. The Q2 growth stood at 4.5%. What has changed since Q2. The growth rate of Q3, FY 18-19 stood at 6.6%.

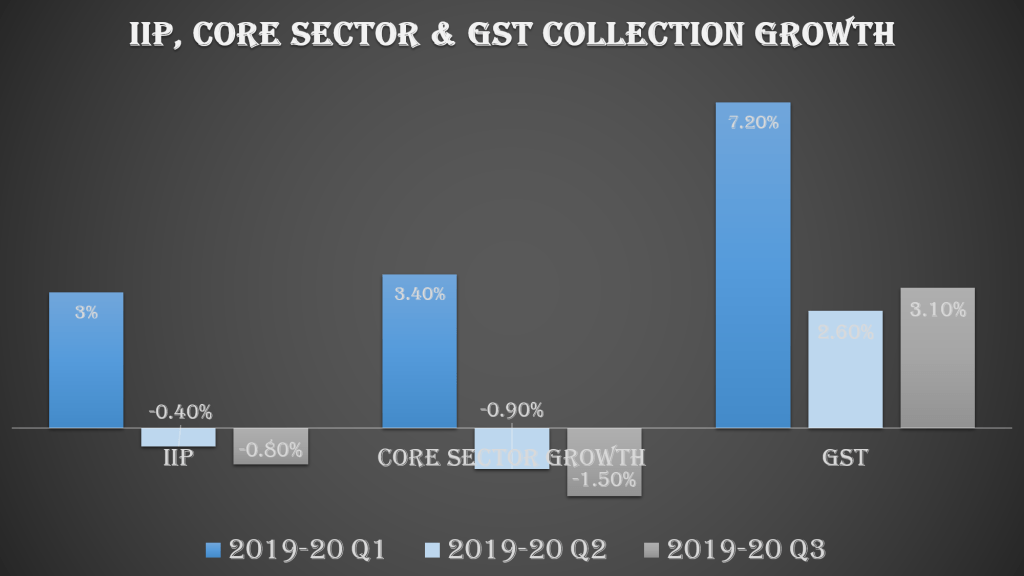

The IIP and the core sector growth numbers showed a steady decline since the first quarter of FY, 2019-20. The decline has been must sharper in Q2 as compared to Q1. The negative trend continued in Q3. There has been a sharper decline in GST collection in Q2, FY 19-20 as compared to Q1 for GST collection growth. The same has seen a marginal increase in Q3. One reason for the increase in GST collection is the step taken by government to cap the input tax credit to 20% to control for revenue leakage. This was announced in October. This might also be suggestive of some surge in demand which saw a sharp decline in the previous quarters.

In terms of sectoral credit growth as reported by Reserve Bank of India, it is seen that almost all the sectors have witnessed a lower credit growth in Q3, 2019-20. The growth rate is significantly lower in almost all the sectors, the most severe being the services sector where it almost has been halved. The only area where there was a marginal growth in the credit growth in the personal credit growth. Personal credit growth is driven by the demand. If we look at the monthly trends it is seen that the highest growth in personal credit was in the month of October, 2019, which happened to be the festive month in India. Since then there has been a decline. But riding on the surge during the festive month we witness a marginal surge in quarter growth number. All the sectoral credit growth numbers are much lower than the growth numbers in the same quarter, last financial year.

The two most prominent factors responsible for slow down in Indian Economy has been the lack of demand and also the slowdown in investments. The Q3, indicators are suggestive of the fact that while the lack of demand is very much there as compared to last year, but when compared quarter on quarter , it has almost remained same with a marginal surge. The sectoral growth numbers are clearly suggestive of the fact that the investment situation has worsen in Q3 as compared to the previous quarters. This is reflective in the decline in IIP and Core sector growth as well

IPD finds that among all the indicators, IIP , growth rate in Personal Credit and Core sector growth has very high correlation with the GDP growth rate. This is followed by the credit growth rate of service sector. Based on all the above indicators IPD forecasts that the GDP growth rate estimates in Q3, FY 19-20 will be between 4.3% – 4.6%.

All major institutions has been conservative in forecasting the growth rate for Indian Economy. NCAER has predicted the growth to be around 4.9% while Motilal Oswal research team has pegged the growth numbers to be closer to 4%. SBI has pegged the growth rate for Q3 to be at 4.3% In terms of YoY growth, Moody’s has reduced the forecast to 5.4%. SBI has predicted 4.7% growth rate in FY 19-20. . The YoY growth rate for FY, 18-19 stood at 6.8%.

Surprising inflation showing upward trend but ironically interest is going down…

LikeLike