Anindya Sengupta

The GDP numbers for April- June, 2020 was announced on 31st August. The country went into a stringent lock down from 25th March. So this quarter began with a near to complete shutdown in economic activity with only the essential services was active. Since April 21st, gradually in phases certain sections of the economy has opened up, however this was very limited initially. Over time the unlock phase began with the economy opening up gradually. So this has been the most deadly quarter in terms of restrictions into economic activity.

Present Performance

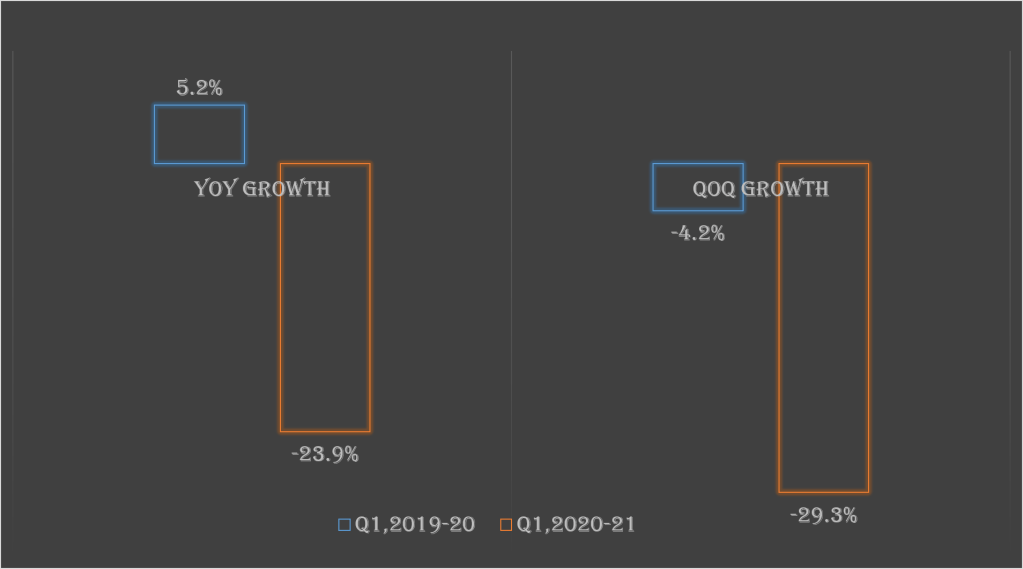

It was widely expected that there is going to be a fall in growth rate. There was consensus that there will be a drop in the growth rate. But what will be the extent of the decline? There were multiple views on the same. Ministry of Statistics and Programme Implementation, Government of India announced that the GDP growth rate ( YoY) has declined to -23.9% as against a 5.2% growth in the same quarter, last year. In comparison with Jan- Mar, 2020, the growth rate declined to -29.2%.

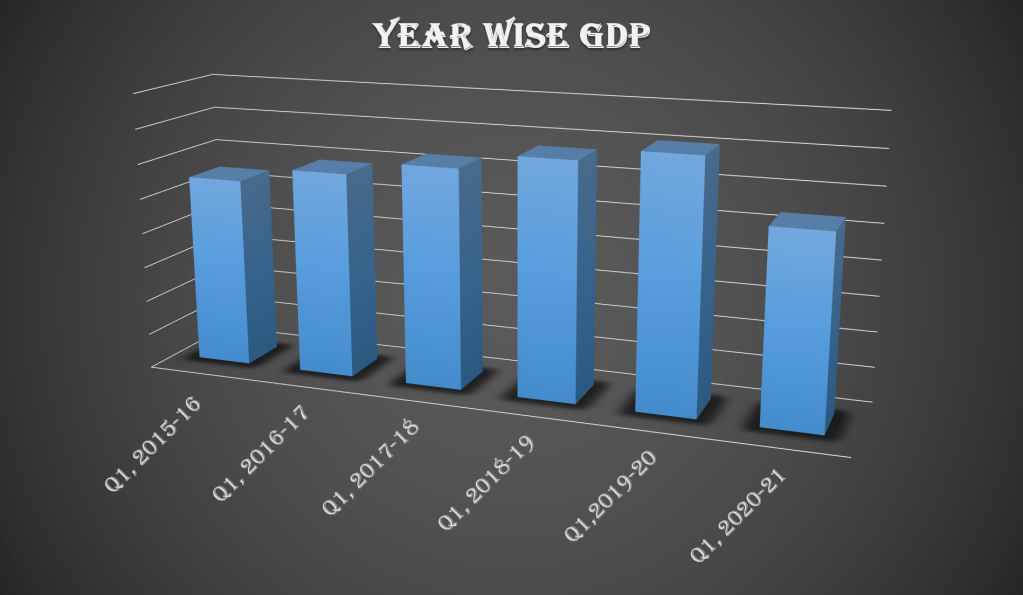

The massive decline of around 24% in the quarter of April-June, lead to a GDP value which is less than the GDP value in this quarter in the last 5 years. The GDP value in this quarter is comparable to the 2015-16, April-June level. So it can be said that the GDP level has leaped back by 5 years given this pandemic.

In order to understand the how will the recovery path be, it is important to understand how resilient the economy was before the advent of COVID and how different sectors performed during the COVID. So a decoding of the performance of the economy is utmost necessary to understand the potential recovery path.

Decoding the Performance of the Economy: PRE-COVID Scenario

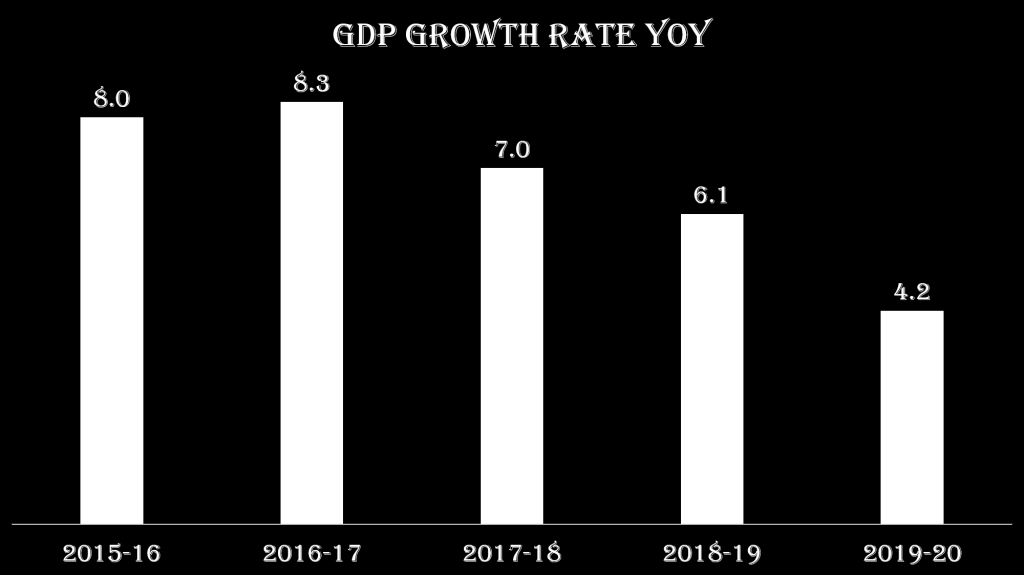

It can be seen that there has been a constant drop in the growth rate from 2016-17 onwards. The GDP growth rate of 2019-20 is the lowest in 11 years. It should be noted here that the impact of the lockdown due to COVID-19 was effective for only 7 days in FY 2019-20. Hence this drop in growth numbers cannot be only due to the lock down. It can be said that Indian Economy was showing a declining trend in the pre-COVID phase itself. It is important to understand why there was a declining trend.

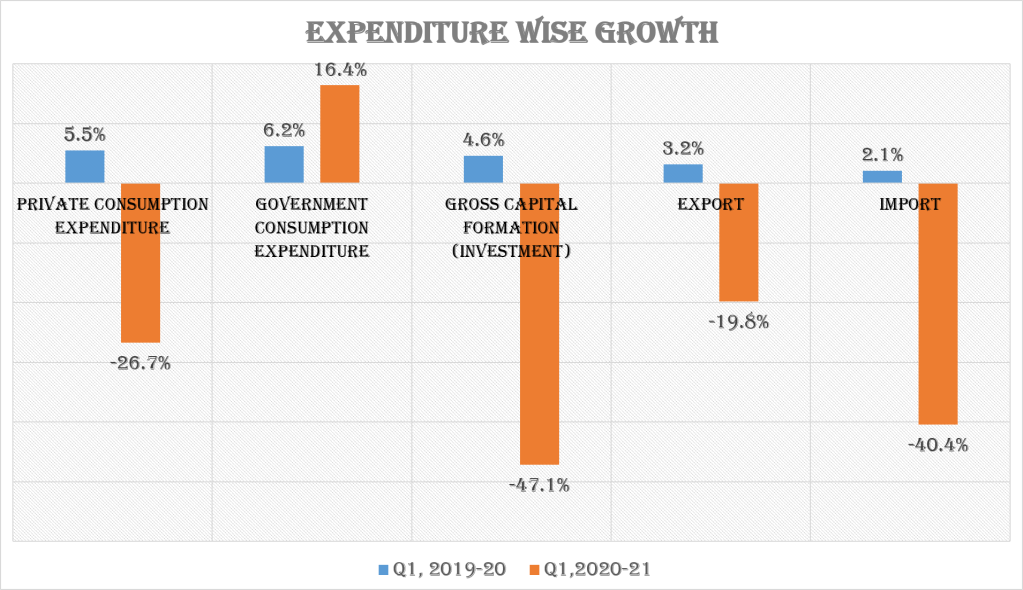

The major component of GDP are the Private Consumption expenditure (a measure for demand) and gross capital formation (a measure for investment). Together they constitute over 87% of the economy. The growth rate of private consumption expenditure has been showing a declining trend for the last few years. Investment growth was negative last financial year (FY 19-20).

Lower growth in demand will mean lower profit for the companies and lower investment. Since the Indian economy has been witnessing a decline in demand growth, this can be in all probability be the reason behind declining growth in investment. Successive governments in India have adopted investment friendly policies. Moreover the government reduced the corporate tax in 2nd quarter, FY 2019-20 in order to boost up investment. In spite of these investment friendly policies there has been a decline in the investment growth in recent past.

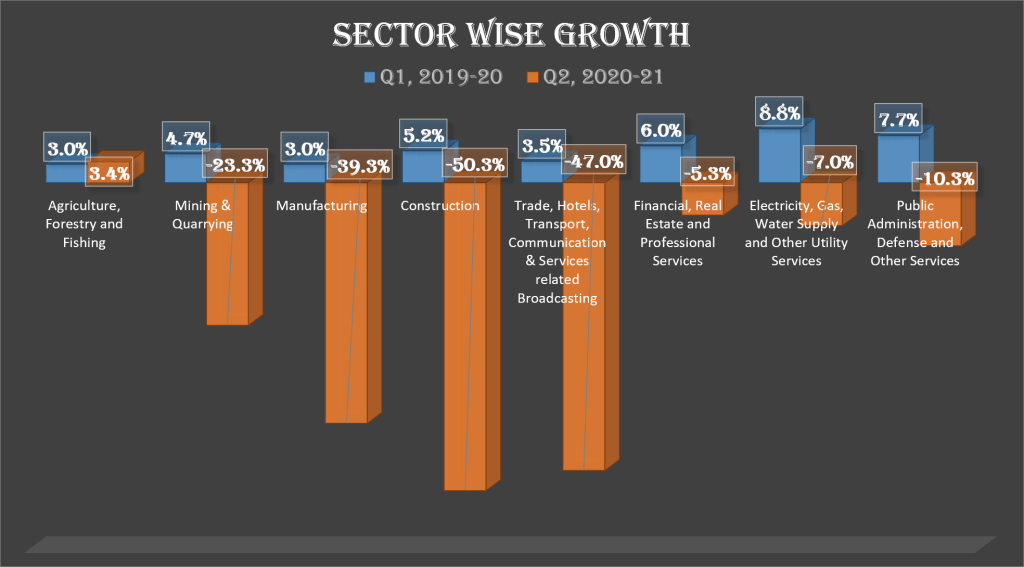

Lower investment leads to slow growth in industrial and services sector. Almost all of the non agricultural sector has witnessed a decline in growth rate in FY 19-20. It should be noted here that manufacturing and construction, the two most people intensive sectors apart from agriculture, witnessed the lowest growth among all sectors. This has a detrimental impact on employment scenario. As per the Annual PLFS data released by the Ministry of Statistics & programme Implementation, the country witnessed the highest unemployment rate in 45 years. This lower investment makes the problem of unemployment more severe.

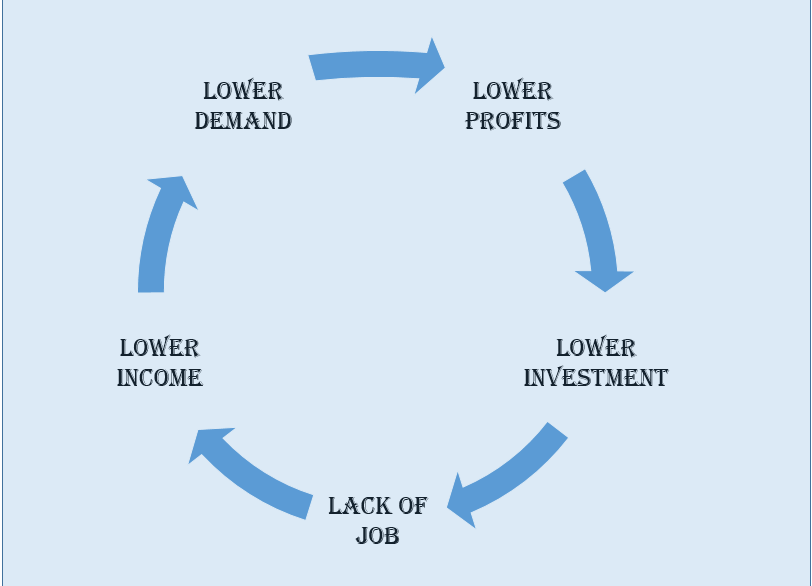

Thus it can be said that both the decline in growth of demand and investment are very much linked to each other and one is leading to the other. This is more alarming given it is a vicious circle.

As is shown, lower demand growth leads to lower profit and hence lower investments. Now lower investments will mean a decline in growth of industrial and services sector leading to lack of jobs in the economy which further leads to lower demand. So a holistic view needs to be taken given this linkage between the lack of growth of demand and that of investment.

Decoding the Performance of the Economy: During the COVID Phase

The economy was witnessing a decline in growth of demand leading to a drop in investment growth. With the advent of COVID, firstly the Indian economy got impacted by the slowdown in China as Indian manufacturing sector has huge dependency on raw materials imported from China. This lead a decline in IIP in the month of March, itself when lock down was there for only 7 days.

With the lockdown, the supply chain got impacted further. With complete stoppage or limited functioning of the economy, both the industrial and the services sector got grossly impacted leading to declining growth in these sectors. The only silver lining was agriculture.

The impact of the lockdown was most severe in people intensive sectors like in manufacturing, construction and Trade, Hotels, Transport, Communication & Services related to Broadcasting. With the people intensive sectors being impacted the most, we also saw a rapid increase in unemployment rate for the month of April and May. With the economy opening up there was some decline in the unemployment rate. Moreover there were reports of significant job cuts across levels as per Centre for Monitoring Indian Economy (CMIE).

The decline in supply and the resultant job loss has lead to further decline in demand which was already impacted in the pre COVID scenario. There has been a significant decline in private consumption demand in the first quarter of FY 20-21.

With the COVID cases on the rise, there has been a slow opening of the economy from the complete lockdown. Further there is a severe decline in demand. Both of these has lead to more uncertainties in the economy. And in uncertain economic environment, investment falls significantly. This is what is seen in the first quarter ( FY 20-21) numbers. The investment growth bears the major burn. With 87% of the economy seeing a significant decline, the overall growth also got impacted. Till the uncertainty prevails there is lesser chance of both investment and demand to grow. In terms of demand, people will tend to hold the money back in such uncertain environment. And with people not spending, there is lesser return to investments, leading to a drop in investment.

Future Outlook

Given this grim picture, what we can expect in the future. The economy has moved out of the stringent lock down. The unlock phase has seen gradual opening of the economy. Still the activity is not at 100%, but definitely higher than what was there in the first quarter. So while there is activity, yet it is less than the normal level. Various organisations has pegged the full year growth figures in the range of -10% to -12% .If we expect a scenario, where from the 2nd quarter onward the GDP value will remain similar to the last year, meaning no growth or fall in GDP for the 3 quarters in this financial year, then our growth will be -5.8% this financial year. This as of now remains the best case scenario.

But how do we get to the best case scenario. The only way is to address the uncertainty. This will require focus on both demand and supply side. That is the optimal way. What is required is

- Universal basic income or some income guarantee policies will ensure that people will have more have more cash in hand and hence they will spend more leading to more profit for industries. This will bring in investment.

- Host of infrastructural projects need to be undertaken. This will boost up the supply side.

- Sufficient liquidity available in the market

The combination of the above measures will help break the vicious circle and will be able to address the steady decline in growth rate. There has host of steps taken to boost the credit and liquidity availability by the government and RBI. But lot needs to be done in the first two aspects. However these measures will mean a rise in government expenditure. The fiscal deficit in FY 19-20 has been 4.6%, higher than the budgeted target. The government needs to rationalize its spending and focus on measures to boost the demand along with boosting the investment. A balance needs to be maintained so that on one hand the fiscal deficit does not rise at an uncontrollable level and on the other hand measures are adopted to help the economy move out of the vicious circle.