Prof Saikat Sinha Roy*

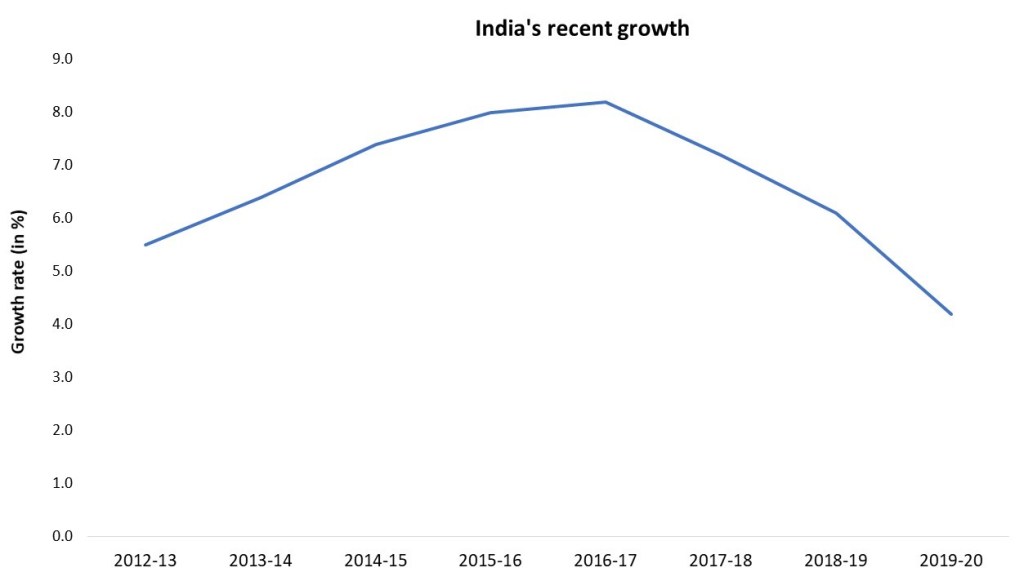

India’s growth rate in GDP has been secularly sliding in recent quarters, the ninth quarter in a row to reach a low rate of 3.1% in the last quarter of 2019-20. This decline follows a slow and fluctuating growth pick up since the beginning of the decade, which peaked in 2016-17, in the second quarter of that year to be specific. The decline since 2016 is sharper than the growth pick-up earlier, and the growth curve for the decade is an inverted V-shaped one!

Such decline in growth actually precedes the economy coming to a screeching halt with lockdown that followed the spread of COVID-19 pandemic – across the length and breadth of the country. With the pandemic related lockdown extending for more than two months, the decline in growth is likely to continue in 2020-21, with the rate expected to be sub-zero in the first two quarters of the year. Even though the pandemic is a one-off event, the decline in growth is not. The decline in growth is structural. The lockdown has just added fuel to the fire and accentuated the growth decline.

India’s growth is private consumption led, and it has stayed all through even in years of slow down. In these years of slowdown since 2016-17, it is somewhat revealing to find that the contribution to growth by gross fixed capital formation, mostly accounted for by private investment, in specific has taken a back seat! Even though the importance of the external sector has increased post globalization, it is not yet and cannot be in the driver’s seat!

In a state of relative “slowdown”, when the economic growth is off the equilibrium path in the short run, demand management, especially revival of private consumption and large-scale public expenditure for income generation, is perhaps the only way to put the economy back on rails. Such demand management is all the more challenging when government revenue generation has hit the rock-bottom, and more public expenditure would run the risk of a larger fiscal deficit.

This is more so when private investment and exports will respectively wait for the domestic economy and the global economy to look up. It is to be noted here that a depreciated rupee will not work to boost exports unless the global market is brighter than it is now. Then, what is the way out of this prolonged decline that culminated into an economy that has hardly any activity?

It needs to be understood at the outset that the character of the economy has undergone a sea change. To borrow from a recent EPW article by Dipankar Dasgupta and Meenakshi Rajeev, the lockdown following the pandemic has transformed a demand constrained economy to a supply constrained one, as was in the case of the infamous Bengal Famine of 1943. Will traditional demand management policies not work in the current situation?

The government has viewed the current economic situation as a supply constrained one, and a myopic view of the situation has pushed the relative stagnation of the Indian economy since 2016-17 into oblivion. The stimulus package thus announced uses this short sightedness and addresses the supply side merely through liquidity injection. Such liquidity would largely be targeted to firms in sectors that are necessarily efficient and where from demand has not shifted out. This is indeed a very lop-sided view even of the supply side.

The supply side issue that needs to be addressed now is resumption of supply of raw materials to the farms and firms, which are often imported into the economy, and bringing back labor to their respective places of work. Mere infusion of liquidity to the economy only presumes that other short run supply constraints in production and distribution will be automatically removed!

Even if raw materials supply, both from within and abroad, resume with a lag, it is unlikely that labor supply to industry and services in the urban sector will resume so soon with the onset of the kharif season and larger expenditure in the rural sector through MGNREGA. Resumption of labour supply, especially migrant labour, comes with a cost. The quick resumption of supply of agricultural commodities and raw materials however does not call for wide ranging reforms with regards to agricultural marketing. Further, the liquidity injection will not generate enough income in the hands of the marginalized and reverse the economic situation in the very short run that follows the lockdown, and not to mention about the prolonged decline that existed prior to the pandemic.

The government thought it to be the opportune moment to move ahead with wide-ranging reforms in land, labor, law and liquidity. As the growth slowdown is observed to be structural in nature, at least to start with, structural reforms are necessary. There are expectations all around, both officially and from unofficial sources, that these reforms will lead to a V-shaped recovery of economic growth. However, reforms necessarily start bearing fruits only after large adjustments over a sufficiently long period of time. The comprehensive reforms since 1991 bears a testimony to that. It is thus doubtful if the current reforms will lead to a V-shaped growth recovery!

The quick resumption of growth, which is a need of the hour, thus requires a mix of income generation policies through massive expenditure in public works programmes both in the rural and urban sectors and resumption of supply of inputs for production and distribution. Putting a limit on public expenditure would mean pushing the economic recovery further. The required reforms can be initiated only once the economy stabilizes. The pertinent question is then whether the much-hyped V-shaped recovery will remain elusive?

* Saikat Sinha Roy is Professor and Coordinator, Centre for Advanced Studies, Department of Economics, Jadavpur University. His fields of specialization are Applied Trade & Development, Open Economy Macroeconomics, Trade Modelling and Applied Economics. He is also a guest faculty at Deptt. of Economics, Calcutta University. Prof. Sinha Roy is the co-editor of the book, International Trade and International Finance: Explorations on Contemporary Issues (2016).

Kindly note that the points of view expressed in this article are entirely the author’s personal views. IPD does not hold any responsibility for the same.

Read this article.

Nice one it is.

Yes, ofcourse.Income generation policies through public expenditure in rural & urban sectors is required now.

LikeLike

Read this article.

Nice one it is.

Yes, ofcourse.Income generation policies through public expenditure in rural & urban sectors is required now.

LikeLike