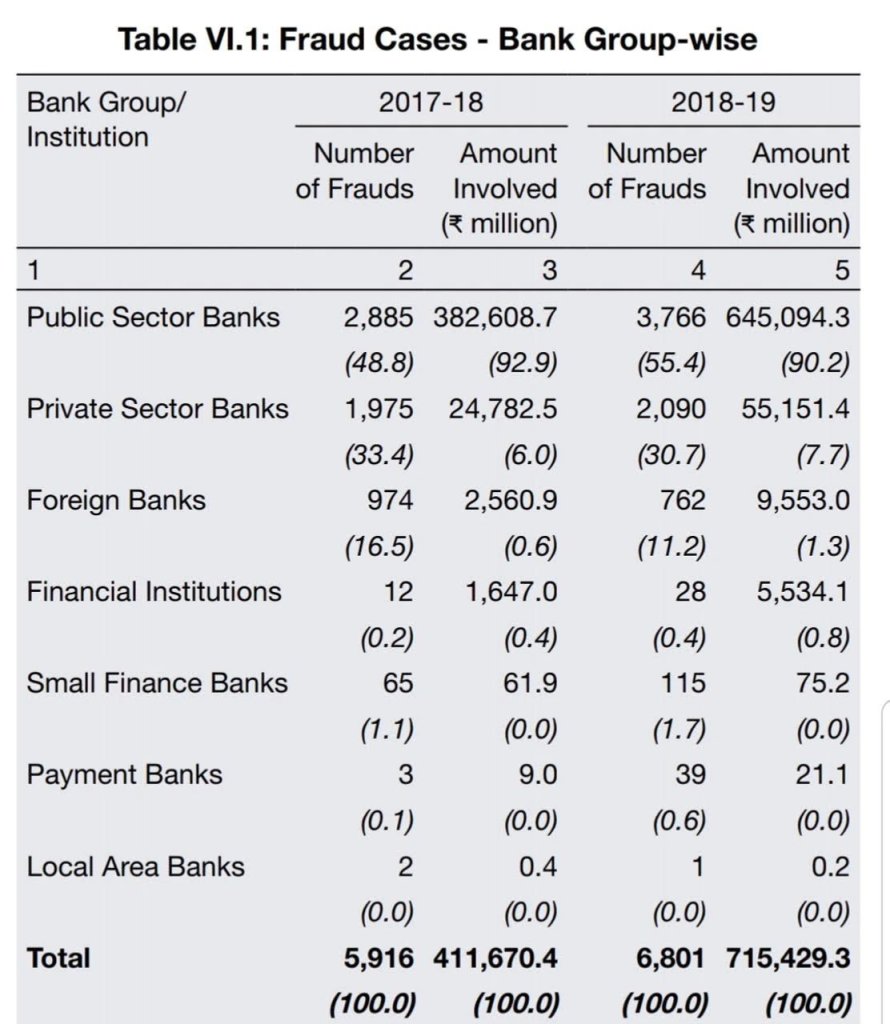

According to the annual report of the Reserve Bank of India (RBI), bank frauds in the country in FY18-19 have gone up (w.r.t FY17-18) by 15% in terms of number of occurrences but by a whopping 73.8% in terms of the amount involved in these frauds. RBI data shows that in FY18-19, banking sector reported 6,801 cases of fraud involving a total Rs 71,542.93 crore as against 5,916 cases involving Rs 41,167.04 crore reported in FY17-18.

The number of cases and amounts involved both have gone up for PSBs as well as private sector banks. Interestingly, foreign banks show a drop in number of occurrences although the amount involved has gone up sharply. A big concern expressed by the RBI is in the time taken for detection of the fraud – standing at an average of 22 months. This goes up to a staggering 55 months (more than 4 & 1/2 years) for large frauds (Rs 1 billion+ amounting to Rs 522 billion). In February’18, after the expose of the Nirav Modi/PNB scam, the RBI and the finance ministry both had set stern guidelines to ensure prevention and early detection of fraud cases. A year later though, facts reveal lack of change at the ground level.

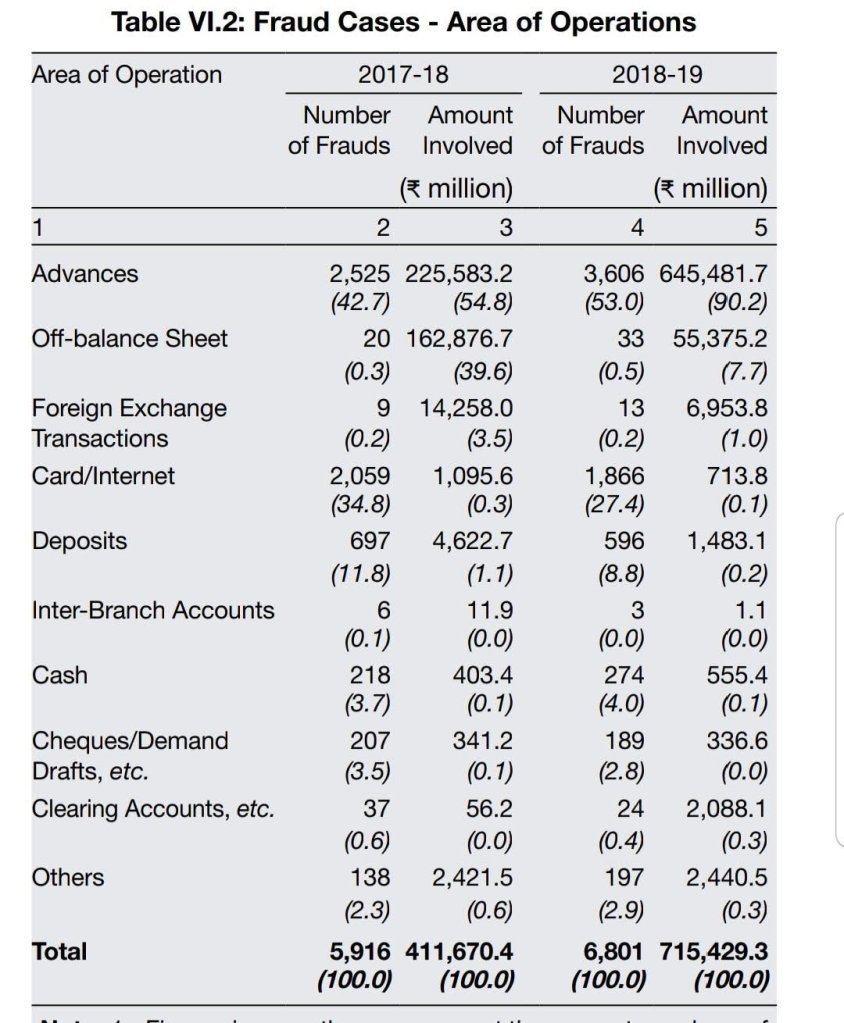

In terms of area of operations, frauds related to advances remained the major share of the total amount involved in frauds while share of this head has gone up sharply in FY18-19, while the share of frauds in off-balance sheet items declined from a year ago.

In terms of no. of cases also, advances were the predominant head followed by cards/internet related frauds. However, share of cards/internet frauds remained minimal in amounts involved.

The RBI said that it is holding discussions with various agencies including the Ministry of Corporate Affairs to create an interlinked database for fraud monitoring. It also stated that analytic engines of banks and user interface of fraud registry would be improved to create a more robust monitoring system. 57 banks were subjected to IT examination by RBI to check their cyber security preparedness and compliances.