The horrible accident of the Coromandel Express, also involving the Yeshwantpur-Howrah Express and a goods train has placed the Indian Railways under a lot of scrutiny. Given that significant part of the Indian Railways infrastructure was constructed during the British era and therefore of ancient antiquity, it makes the regular inspection and maintenance of the tracks and other ancillaries extremely critical for safety and security.

In this respect, we decided to make a series of reviews on the maintenance of assets at Indian Railways. In this, our primary source is the “Report of the Comptroller and Auditor General of India for the year ended March 2021: Derailment in Indian Railways.”

Part I, reviewing track and other asset maintenance status was published earlier. This is Part II.

Disclaimer: These review articles do not make any attempt to investigate causes of the tragic accident at Balasore last week. These are reviews of the adherence on ground to the prescribed practices for safety and security by the Ministry of Railways from multiple angles. They cover the period of 4 years from April 2017 – March 2021.

Rashtriya Rail Suraksha Kosh (RRSK)

In the Budget Address of 2017-18, the Ministry of Railways (MoR) announced the creation of the Rashtriya Rail Suraksha Kosh (RRSK) with a corpus of Rs 1 lakh crores. The mandate of RRSK was to finance critical safety related works of track renewal, replacement and augmentation of IR assets.

The funding of RRSK was described as follows: Corpus of Rs 1 lakh crores to be created over five years – annual outlay of Rs 20,000 crores. 75% i.e. Rs 15,000 crores from Gross Budgetary Support and 25% i.e. Rs 5000 crores from Railways’ internal resources.

The CAG Audit finds that from 2017-18 to 2020-21, while the Gross Budgetary Support annual contribution of Rs 15,000 crores has been contributed; there are major shortfalls in Railways’ contribution of Rs 5000 crores. The year-wise shortfall is given in the below table:

As can be observed, there is a nearly 80% shortfall in Railways’ planned contribution to the RRSK. Since the stated mandate of RSSK was to fund critical expenditure related to infrastructure safety, this major shortfall is a big blow to that effect

It is thus little wonder that the Standing Committee of Railways observed that “the purpose of RRSK is gradually being eroded due to non-appropriation of required funds from internal resources of Railways”

Priority utilization of RRSK

In December, 2015, an Internal Committee of senior MoR officials estimated a budget of Rs 154,000 crores for spending on a range of inter-departmental safety initiatives. It was estimated that Rs 119,000 crores was to come from RRSK. Since RRSK’s corpus was kept at Rs 1, 00,000 crores, thus implying that entire safety work recommended by the internal committee could not be carried out from RRSK funding.

In February’17, the MoR requested NITI Aayog to help identify critical areas and guiding principles to prioritize RRSK funds in order to effect perceptible improvement in safety management of IR. In July’17, the Ministry of Finance based on NITI Aayog recommendations, issued guidelines on utilization of RRSK funds by MoR. It was made explicit that strict adherence to above guidelines was mandatory for implementation of railway safety works out of RRSK funding.

The priority areas for expenditure were narrated as below:

Priority I: Civil engineering works for minimizing derailments and Level crossing related works

Priority II: Electrical & Mechanical engineering works that target minimizing derailments

Priority III: Initiatives targeted at reducing probability of human errors in critical areas of operation

The MoR had thus instructed mandatory adherence to above priority hierarchy as far as utilization of RRSK funds.

The CAG Audit for the years 2017-18 to 2019-20 finds the actual utilization as below:

Expenditure on Priority I heads declines in absolute terms from Rs 13, 652 crores in 2017-18 to Rs 11, 655 crores in 2019-20

In percentage terms, it drops from 81.55% to 73.76%

Conversely, expenditure on Non-priority items rose from Rs 463 crores (‘17-‘18) to Rs 1004 crores (’19-’20) – in % terms from 2.76% to 6.36%

In the year 2018-19, two zones: CR and WR spent 12-13% of RRSK funds on non-priority areas

Increasing expenditure on non-priority areas at the cost of Priority I heads defeats the fundamental purpose of RSSK funds.

Expenditure on Track Renewals

Tracks are the backbone of any railway system. Thus, track maintenance and renewal both are absolutely imperative tasks for railway management.

“Indian Railway has a network of 1, 14,907 KMs of which 4500KMs track should be renewed annually” ~ White Paper on IR (2015).

In this respect, below are some of the pertinent observations made by the CAG Audit:

In eight railway zones (ZRs), expenditure on track renewal showed a declining year-on-year trend from the time RRSK was introduced

Allotment of funds (Final Grant) for Track Renewal works declined from Rs 9607.65 crores (2018-19) to Rs 7417 crores (2019-20)

In 2017-18, seven ZRs surrendered funds to the tune of Rs 299 crores. In 2018-19, nine ZRs surrendered total Rs 162.85 crores fund. In 2019-20, five ZRs surrendered Rs 11.68 crores

The trend of declining fund allocation and non-utilization of allocated funds is a cause of concern more so as the Audit found that 26% of derailments during the 3-year audit period could be directly attributed to non-renewal of tracks.

Expenditure booking in RRSK

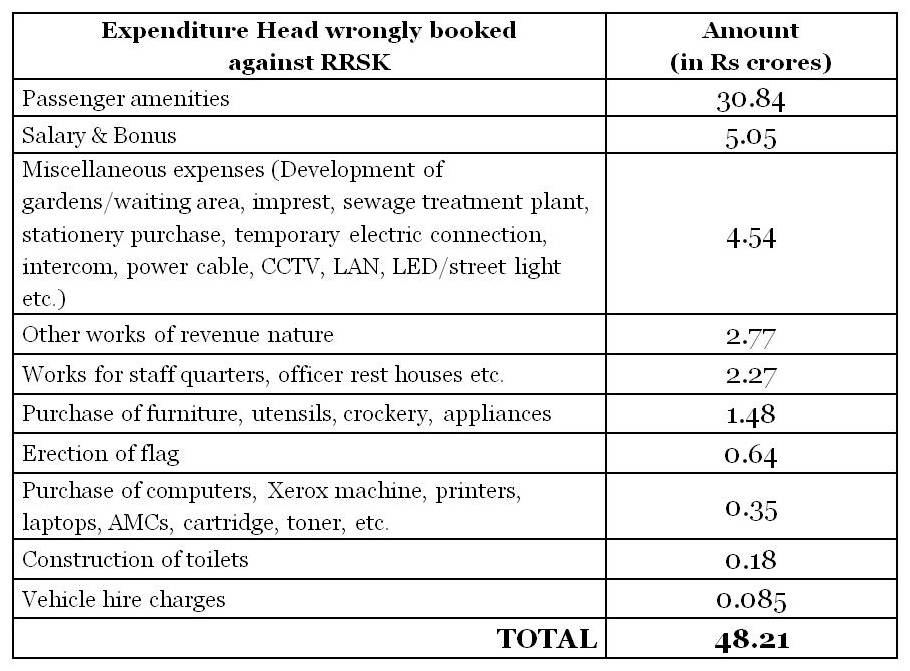

The audit did a random check of vouchers pertaining to RRSK for one month of each of the four years under review in two selected divisions of each ZR.

Vouchers amounting to Rs 2995.58 crores, booked under RRSK were audited and it was found that vouchers amounting to Rs 48.21 crores were not pertaining to the three Priority areas as set by MoR. Details of the same are given below:

Utilization of RRSK funds for revenue expenses when the same was explicitly made mandatory for utilization in priority I/II/III areas is a serious procedural lapse. Also, the above is result of audit of just 4 months out of 38. A total audit would obviously reveal lapse at a much larger scale.

Conclusion

The Audit findings on mobilization and utilization of RRSK funds are a cause of major concern. The objectives of creation of a dedicated fund for financing works targeted at improving rail safety are defeated if the expenditure is not monitored and used / utilized for non-priority heads.

Moreover, the failure of Railways to contribute the mandated amount for all the four years is a huge and glaring omission of duty that is certainly having an adverse impact on rail safety.

(To be continued)